|

1

|

|

|

2

|

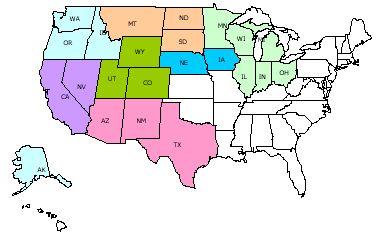

- A Diversified Financial Services Company:

- Focused on banking, insurance, investments, mortgages, and consumer

finance

- Wells Fargo Bank covers 23 states

- Coverage includes 12 of the nation’s fastest growing states

- Includes key ethnic minority population states: California, Colorado, Texas, New

Mexico, Arizona, and Nevada

- Wells Fargo Financial covers the majority of United States and also

features an international presence in Canada, Latin America and the

Caribbean

- Wells Fargo Home Mortgage covers the the entire United States and

features the most extensive franchise of the company

|

|

3

|

- Key Wells Fargo Ratings:

- Only “Aaa” rated bank by Moody’s in the US

- #5 US bank with $388 Billion in Assets (12/31/03)

- #1 Total stores with 5,900 stores

- #3 Bank with 3,021 stores

- #1 Supermarket bank with 680 stores

- #3 ATM Network with 6,192 ATMs

- #1 Mortgage bank with an additional 997 stores

- #4 Consumer finance company with 1,221 stores

|

|

4

|

|

|

5

|

|

|

6

|

|

|

7

|

|

|

8

|

|

|

9

|

- Consumer Remittance Opportunity:

- US International remittance market is currently estimated at $50 Billion

- Concentration:

- Mexico remittances market is $14 Billion

- Indian remittances market is $11 Billion

- Latin America & Caribbean remittance market is $32 Billion (2002)

- 69% of all Latinos living in the US send remittances (Bendixen 2002)

- 75% of all Latino remittances come from the United States (Orozco 2003)

- 44% of all Latinos lack bank accounts in the US (SRC 2002)

- Non-Banks Dominate the Market:

- 45% of remittances are processed by informal networks

- Banks share of remittance business is estimated at 9% (Nilson) and 16%

(Celent)

- More than 50% of total volume is distributed by financial institutions

offshore (Orozco 2003)

|

|

10

|

|

|

11

|

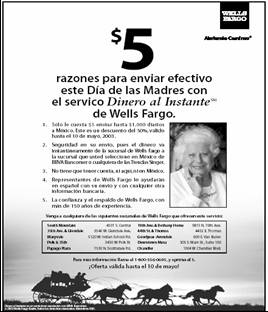

- Mexican Matrícula Consular Card accepted as valid Identification for

account opening process

- No minimum balance requirements

- No initial deposit required

- Transfers can be initiated at the bank branch, ATM, over the phone or

online

- Only $10 fee per transfer for up $3,000 per transfer/per day

- No monthly account maintenance fees

|

|

12

|

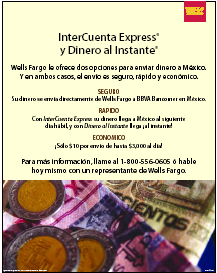

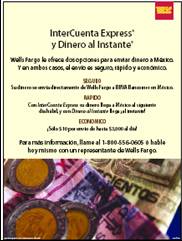

- Security: Secure transfer from

the Wells Fargo account to the beneficiary’s bank account abroad. There are no intermediaries.

- Convenience: Account access is available 24 hours a

day, over the telephone, online

or at thousands of Wells Fargo Bank locations and ATMs

- Distribution: Largest Direct

Distribution of any US Bank:

- BBVA Bancomer features the largest branch network distribution Mexico

with over 1,600 branch locations and 3,700 ATMs throughout the country.

- HSBC Mexico features one of Mexico premier distribution networks with

over 1,400 branch locations and 4,500 ATMs throughout the country.

|

|

13

|

|

|

14

|

|

|

15

|

|

|

16

|

|

|

17

|

|

|

18

|

- “We’re proud to have been the

first major financial services company in the United States to help

Mexican nationals move from the risky cash economy into secure and

reliable financial services – by promoting acceptance of matrícula card

as a primary form of identification.”

- October 24, 2003

- Dick Kovacevich

- Wells Fargo, Chairman and CEO

|

|

19

|

- It’s the people that make the difference!

- Wells Fargo banker and teller initially drive the customer relationship

- In Mexico, the BBVA Bancomer or HSBC Mexico banker and tellers provide

a personal touch

- ATM, Internet, and Telephone are transaction and self-service channels

|

|

20

|

|

|

21

|

- All product materials available in language

- Adjusted store formats to appeal to the local community

- All channels offer in language service (ATM, Online, Phone Bank)

- Local level community advisory boards

- Local decision making and execution

|

|

22

|

- Promotional vs. Brand Image Campaigns

- Locallly driven focus (grass roots)

- Community group partnerships

- Consular offices

- Financial literacy programs

|

|

23

|

|

|

24

|

- Above avg. cross sell level : Exceeds 4.2 product cross sell (company

average)

- Above avg. remittances: $600+/remittance

- Double digit growth in transaction volume and value

- High satisfaction scores with customer base with high referral potential

|

|

25

|

- Increased Household Acquisition

- Increased product cross sell

- Long term relationships

- Loyalty effect -> Referral & Retention

- Sustained growth

|

|

26

|

|

|

27

|

- Banks and community groups must develop and facilitate financial

literacy programs to provide the appropriate exposure to financial

products. Here are some examples:

- Matricula Consular Guide (Financial literacy pamphlet) currently

distributed by all of the Mexican Consulates and funded by major

financial institutions in the US

- Financial literacy programs such as:

- www.handsonbanking.org

- www.elfuturoentusmanos.org

- Bancarization efforts must be bilateral (sending and receiving banks

must be equally focused)

- Foreign governments may consider incentives and benefits for both large

and small financial institutions

- Provide enhanced access (more convenient bank and ATM locations)

- Product development focus (simplified products/low cost)

- US case: CRA recognizes distribution and product focus

|

|

28

|

- Wells Fargo has opened over 400,000 accounts with the Matricula Consular

in the United States

- Banks in Latin America and the Caribbean may consider ways to simplify

the documentation requirements

- In the US, most banks only require two forms of ID and a Social

Security number (SSN) or Individual Tax Payer Identification number

(ITN)

- Banks in Latin America and the Caribbean must look for ways to simplify

and streamline the new account opening process and related personal

identification/documentation

requirements in order to simplify the process.

- Limit account opening requirements

- Simplify the account opening application form

- Reduce fixed costs associated with minimum balances, etc

- Banks in Latin America and the Caribbean may consider low cost

alternatives to initial low transaction (lower cost) activity accounts

opened by remittance recipients

|

|

29

|

- Card based solutions are one of the ideal vehicles for remittances in

Latin America and the Caribbean in the future

- The near term effectiveness of this remittance vehicle is limited by the

following factors:

- Limited ATM distribution in the rural areas

- In major cities, ATMs are predominant in the business districts and

somewhat limited in the residential low to middle income districts

- Card acceptance at retail consumer outlets in Latin America is growing

at a incredibly fast pace.

Distribution must continue to grow.

- The retailer’s costs associated with processing card transactions in

Latin America requires further analysis

- ATM security and safety must be guarded in order to guarantee safety to

the remittance recipient

|

|

30

|

- Consumer awareness of lower priced remittance product alternatives with

banks is a key challenge

- Local media and community organizations must play a role

- Independent party cost comparisons of existing products and associated

pricing are needed for remittances:

- Mexico: PROFECO provides a

weekly cost comparison

- Cost comparisons should be made at the low end and high end

transaction amount levels ($200, $500, $1,000, $1,500)

- Cost comparison information should be provided in print media and

published by consumer advocacy groups

- Partial savings of remittances should be encouraged by sending and

receiving institutions to promote productive use of remittance in the

form of new venture capital and/or educational investments.

- The productive use of remittances will enhance the long term financial

position of the remittance receiver

|

|

31

|

- Daniel I. Ayala

- Senior Vice President

- Cross Border Payments Manager

- 925.686.7466

- [email protected]

|

|

32

|

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}